In

these days of economic uncertainty it is essential that people

have a sense of security and peace in terms of their future. Long

term care insurance is a way to help preserve that.

"Your future will happen whether you plan for it or not." |

|

The most frequent questions are:

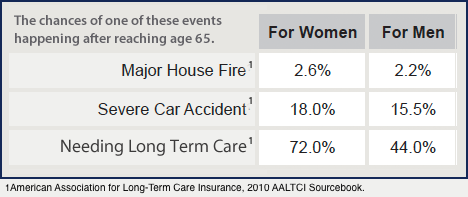

"Will I ever need long term care?"

The fact that this cannot be known in advance and can happen at any time creates the necessity for planning.

How much notice do we get when our health changes? You may be insurable today but not tomorrow.

The Govt. Accounting Office predicts that 70% of Americans over 65 will need long term care. Long term care needs will only increase with the aging boomer population.

"How much does long term care insurance cost?"

Like other insurance it depends on how much of the risk you want to insure. Your age, health and benefits you choose will determine the premium. We can help you design the most appropriate and affordable plan.

Since we represent the major California insurance companies, the premiums will be the same if you buy your insurance through us or somewhere else. As independent brokers we work for you, not the insurance company.

For some people traditional long term care insurance might not be the best choice or maybe they can't health qualify.

At California LTC we offer multiple solutions for every financial and health situations: long term care insurance, hybrid life insurance with a long term care rider and a deferred annuity with a long term care rider.

With our quote service you will get competitive quotes from the different long term care insurance companies.

When you request an insurance quote you will receive quotes and brochures from the top companies. The policy you purchase from us is usable in any state.

Contact us if you have any questions.

|

PH: 707-479-3259

NPN 7595504 – CA Lic. 0D90327

Mail: PO Box 5894, Petaluma, CA 94955

|

|

|

|